First Home Buyer’s Guide to St George: Buy with $35K in 2026

How government schemes, smart suburb selection, and expert guidance make homeownership achievable with less than you think

I still remember the couple I helped last month — Sarah and Tom, both 28, sitting in my office with a mix of excitement and terror on their faces.

“We’ve been saving for three years,” Sarah said. “But we’re nowhere near the $100,000 everyone says we need.”

I smiled. I’ve had this conversation hundreds of times in my 25+ years as a St George real estate agent.

“How much do you have saved?” I asked.

“About $37,000,” Tom replied, looking defeated.

“Perfect,” I said. “That’s more than enough.”

Their faces lit up with disbelief.

Three weeks later, they had the keys to a beautiful 2-bedroom unit in Banksia. They used the First Home Buyer Assistance Scheme, paid zero stamp duty, and their deposit was just 5% thanks to the government guarantee.

This is happening every week in St George.

If you think homeownership is out of reach, I’m here to show you it’s not. Let me break down exactly what you need, where to buy, and how to navigate the 2026 first home buyer landscape.

The Money: What You Actually Need (It’s Less Than You Think)

The Old Rule vs The New Reality

Your parents’ generation needed 20% deposit, paid stamp duty in cash, and dealt with mortgage insurance. That’s not your reality in 2026.

Here’s what’s changed:

What Your Parents NeededWhat You Need in 202620% deposit5% deposit (with government guarantee)Stamp duty in cash$0 stamp duty (if you qualify)Mortgage insuranceNo mortgage insurance (with the right scheme)

Real-World Examples: What You’ll Actually Pay

Let me show you three real examples from St George suburbs:

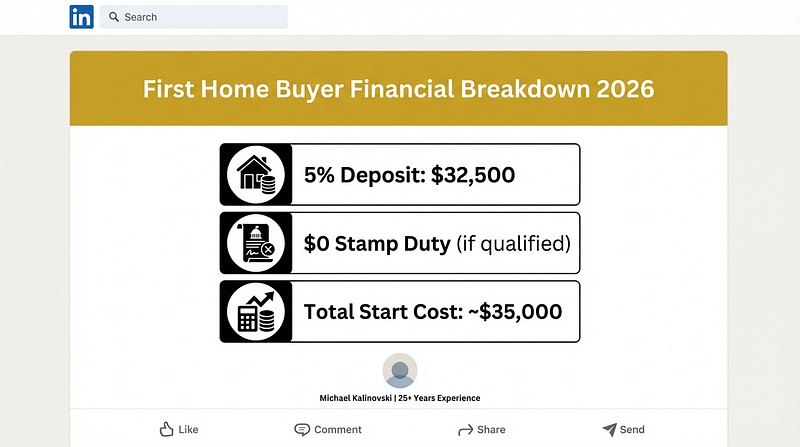

Example 1: Unit in Banksia

- Purchase Price: $650,000

- 5% Deposit: $32,500

- Stamp Duty: $0 (first home buyer exemption)

- Legal Fees: ~$2,000

- Building Inspection: ~$500

- Total Upfront Cost: ~$35,000

Example 2: Unit in Arncliffe

- Purchase Price: $620,000

- 5% Deposit: $31,000

- Stamp Duty: $0 (first home buyer exemption)

- Legal Fees: ~$2,000

- Building Inspection: ~$500

- Total Upfront Cost: ~$33,500

Example 3: Unit in Rockdale

- Purchase Price: $700,000

- 5% Deposit: $35,000

- Stamp Duty: $0 (first home buyer exemption)

- Legal Fees: ~$2,000

- Building Inspection: ~$500

- Total Upfront Cost: ~$37,500

The Bottom Line: With $35,000-$40,000 saved, you can realistically buy in St George.

NSW First Home Buyer Assistance: Your Secret Weapons

The 2026 government schemes are game-changers. Here’s what’s available:

1. First Home Buyer Assistance Scheme (Stamp Duty Exemption)

This is the big one. If you qualify, you pay zero stamp duty on properties under $800,000.

Who Qualifies:

- First home buyer (never owned property in Australia)

- Australian citizen or permanent resident

- Must live in the property for at least 6 months

- Property value under $800,000

What You Save:

Property PriceStamp Duty Saved

$600,000 — $24,240

$650,000 — $26,990

$700,000 — $29,740

$750,000 — $32,490

$800,000 — $31,190

Real Talk: This is FREE MONEY. A $650,000 unit saves you nearly $27,000 in stamp duty. That’s a year’s worth of savings for many people.

2. First Home Guarantee (5% Deposit Scheme)

This scheme lets you buy with just 5% deposit and no mortgage insurance.

Who Qualifies:

- First home buyer

- Australian citizen or permanent resident

- Individual income under $125,000 (or $200,000 combined for couples)

- Property value under $800,000 in Sydney

What You Save: Lenders Mortgage Insurance (LMI) on a $650,000 property with 5% deposit would typically cost $15,000-$20,000. With this scheme, you pay $0.

3. First Home Super Saver Scheme

This one’s clever. You can use your superannuation to save for your first home.

How It Works:

- Make extra contributions to your super (up to $15,000 per year)

- Withdraw up to $50,000 (plus earnings) for your first home

- Tax benefits on contributions and withdrawals

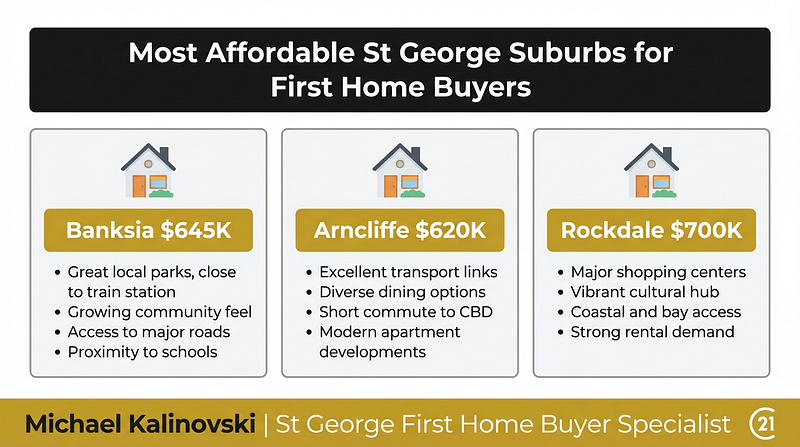

The Most Affordable St George Suburbs for First Home Buyers

Not all St George suburbs are created equal. Here’s where your money goes furthest:

Tier 1: Most Accessible Entry Points

Banksia (Median Unit Price: $645,000)

Why It Works:

- Under the $800,000 stamp duty threshold

- 5-minute walk to Rockdale station

- Quiet, residential streets

- Growing café scene on Princes Highway

What You’ll Get:

- 2-bedroom units: $600K-$700K

- Older-style units with renovation potential

- Some with parking and storage

- Strong rental demand (backup plan if needed)

The Banksia Advantage: This is where Sarah and Tom bought. It’s not flashy, but it’s solid, affordable, and well-connected. In 5 years, the area’s transformation will make early buyers look very smart.

Arncliffe (Median Unit Price: $620,000)

Why It Works:

- Most affordable suburb in St George

- Undergoing significant transformation

- Train station on your doorstep

- Future growth potential as area develops

What You’ll Get:

- 2-bedroom units: $580K-$680K

- Mix of older walk-ups and newer buildings

- Some with parking included

The Arncliffe Opportunity: This is the “emerging” suburb play. It’s not perfect now, but the bones are good. Train station, proximity to airport, and ongoing development make it a smart long-term choice.

Rockdale (Median Unit Price: $700,000)

Why It Works:

- Major transport hub (train and bus)

- Established amenities and shopping

- 2km from Brighton-Le-Sands beach

- Strong rental demand

What You’ll Get:

- 2-bedroom units: $650K-$750K

- Mix of older and modern buildings

- Better amenities than Banksia or Arncliffe

The Rockdale Balance: You pay a bit more, but you get more established infrastructure. Good middle ground between affordability and lifestyle.

Tier 2: Stretch Suburbs (If You Have More Saved)

Kingsgrove (Median Unit Price: $750,000)

Family-friendly with good schools nearby. Worth considering if you have $40K+ saved.

Carlton (Median Unit Price: $700,000)

Residential feel with parks and green spaces. Quieter than Rockdale but similar price point.

The Step-by-Step First Home Buying Process

Let me walk you through exactly what happens, from first thought to holding keys.

Step 1: Get Your Finances Sorted (2–4 weeks)

Action Items:

- Check your credit score (free through various services)

- Gather 3 months of payslips

- Collect 3–6 months of bank statements

- Calculate your genuine savings (must be held for 3+ months)

- Reduce unnecessary expenses to show good financial habits

Pro Tip: Lenders look at your spending habits. That $200/month on Uber Eats? They notice. Clean up your spending 3–6 months before applying.

Step 2: Get Pre-Approved (1–2 weeks)

Why It Matters:

- Determines your exact budget

- Enables quick decision-making at inspections

- Avoids falling in love with unaffordable properties

- Shows sellers you’re a serious buyer

Pro Tip: Get pre-approved for slightly more than you plan to spend. It gives you negotiation flexibility.

Step 3: Start Your Property Search (2–8 weeks)

Must-Haves:

- Within your pre-approved budget

- Close to transport (walking distance to station)

- Secure parking (essential in Sydney)

- Reasonable strata fees (<$1,500/quarter)

Nice-to-Haves:

- North-facing living areas

- Outdoor space (balcony or courtyard)

- Storage

- Modern kitchen and bathroom

Pro Tip: Attend 10–15 inspections before making an offer. You’ll quickly learn what’s good value and what’s overpriced.

Step 4: Make an Offer (1 day — 1 week)

Auction vs Private Treaty:

AuctionPrivate TreatySet date and timeNegotiate directly with agentCompetitive bidding5-day cooling-off period (NSW)No cooling-off periodMore time to arrange financeTransparent processPrivate negotiations

Pro Tip: For first home buyers, I usually recommend private treaty. The cooling-off period gives you peace of mind and time to finalize everything.

Step 5: Exchange Contracts (1–2 weeks)

What Happens:

- You pay 10% deposit (e.g., $65,000 on a $650,000 property)

- Contracts are signed by both parties

- Cooling-off period begins (if private treaty)

- Building and pest inspections completed

Pro Tip: Never skip building and pest inspections. I’ve seen buyers save tens of thousands by discovering issues before exchange.

Step 6: Settlement (4–6 weeks after exchange)

Key Activities:

- Final loan approval from bank

- Final inspection of property

- Transfer of ownership

- You receive the keys!

Common First Home Buyer Mistakes (And How to Avoid Them)

In 25+ years, I’ve seen these mistakes repeatedly. Learn from others:

Mistake #1: Buying at the Top of Your Budget

The Problem: You get approved for $700K, so you buy at $700K. Then interest rates rise, or you have unexpected expenses, and you’re financially stressed.

The Solution: Buy $50,000-$100,000 below your maximum. This buffer protects you from rate rises and life’s surprises.

Real Example: I had clients approved for $750K who bought at $650K. When rates rose 1%, they were comfortable. Their friends who maxed out their budget? Struggling.

Mistake #2: Skipping Building and Pest Inspections

The Problem: You save $500-$800 on inspections. Then discover $20,000 in structural issues after settlement.

The Solution: Always get professional inspections. Always.

Real Example: A building inspection revealed $15,000 in water damage in a unit. The buyers negotiated a $15,000 price reduction. Best $600 they ever spent.

Mistake #3: Ignoring Strata Fees and Ongoing Costs

The Problem: You focus only on the mortgage payment and forget about strata fees, council rates, water, insurance, and maintenance.

The Solution: Calculate total monthly costs before buying.

Real Example: A couple bought a unit with $600/quarter strata fees. Seemed fine. Then they discovered a $50,000 special levy for building repairs. Always check the strata report.

Mistake #4: No Emergency Fund After Settlement

The Problem: You use every dollar for deposit and settlement costs. Then the fridge breaks, or you lose your job, and you have no buffer.

The Solution: Keep $5,000-$10,000 in savings after settlement for unexpected expenses.

Monthly Costs: What You’ll Actually Pay

Let’s break down the real monthly costs for a typical first home buyer in St George.

Example: $650,000 Unit in Banksia

Mortgage Payment:

- Loan amount: $617,500 (5% deposit)

- Interest rate: 6.5% (current average)

- Loan term: 30 years

- Monthly payment: ~$3,900

Other Monthly Costs:

ExpenseMonthly CostStrata fees$450Council rates$140Water rates$60Building insurance$40Total~$4,590/month

Reality Check: This is tight for a single buyer but very achievable for a couple with combined income of $90K-$100K each.

Smart Strategies for St George First Home Buyers

Strategy #1: Buy with a Friend or Sibling

How It Works: Two buyers pool their deposits and incomes. This doubles your buying power.

Example:

- You have $20K saved, your friend has $20K

- Combined: $40K deposit

- Combined income: $180K+

- You can afford a $700K+ property together

Pro Tip: Get a solicitor to draft a co-ownership agreement before buying. It protects both parties.

Strategy #2: Buy in an “Emerging” Suburb

The Concept: Buy in suburbs that are currently affordable but have strong growth indicators.

St George Examples:

- Arncliffe: Undergoing transformation, train station, airport proximity

- Banksia: Growing café scene, improving amenities, good transport

Pro Tip: Look for suburbs with infrastructure investment (new train stations, shopping centers, parks).

Strategy #3: Cosmetic Renovation for Instant Equity

The Concept: Buy an older, dated unit at a discount. Spend $20K-$30K on cosmetic renovations. Increase value by $50K+.

Focus Areas:

- Fresh paint (biggest impact for lowest cost)

- Kitchen upgrade (new benchtops, cabinet doors, appliances)

- Bathroom refresh (new fixtures, tiles, vanity)

- New flooring (laminate or vinyl plank)

Example:

- Buy: $580K (dated unit in Banksia)

- Renovate: $30K (cosmetic only)

- New value: $650K+ (after 6 months)

- Instant equity: $40K+

Pro Tip: Don’t over-capitalize. Stick to cosmetic changes that give maximum return.

Frequently Asked Questions

Q: Can I buy with less than 5% deposit?

A: Technically yes, with guarantor loans (parent guarantees part of your loan). However, the 5% First Home Guarantee is the most common and recommended path.

Q: What if I’ve owned property overseas?

A: You’re still eligible for first home buyer schemes if you’ve never owned property in Australia. Overseas ownership doesn’t disqualify you.

Q: Should I buy alone or with a partner?

A: Financially, buying with a partner is easier (combined income and deposit). However, consider a legal agreement before purchasing together, especially if not married.

Q: How long does the whole process take?

A: From starting your search to holding keys: typically 3–6 months. Can be faster if you’re pre-approved and find the right property quickly.

Q: What if interest rates rise after I buy?

A: This is why I recommend buying below your maximum budget. Build in a buffer for rate rises. Also consider fixing part of your loan for certainty.

Q: Can I rent out a room to help with mortgage?

A: Yes, but check your loan conditions and strata bylaws. Many first home buyers rent out a room to offset costs.

Your First Home Buyer Action Plan

Here’s your month-by-month roadmap:

Month 1–2: Preparation Phase

- Research suburbs (attend open homes on weekends)

- Check credit score and fix any issues

- Start saving aggressively

- Reduce unnecessary expenses

Month 3: Get Serious

- Engage a mortgage broker

- Get pre-approved

- Narrow down to 2–3 target suburbs

- Attend 5+ open homes per week

Month 4–6: Active Search

- Attend inspections regularly

- Make offers on suitable properties

- Negotiate with agents

- Complete building inspections

Month 7: Exchange and Settlement

- Exchange contracts

- Final inspections

- Arrange removalists

- Settle and receive keys!

Why Work with a Local Expert

After 25+ years in St George, I know:

- Which streets flood and which don’t

- Which buildings have issues and which are solid

- Which agents are honest and which overprice

- Which suburbs are genuinely improving

I have connections to:

- Mortgage brokers who specialize in first home buyers

- Solicitors who won’t overcharge

- Building inspectors who are thorough

- Tradespeople for renovations

Most importantly: I provide no-pressure guidance. First home buying is stressful enough without a pushy agent.

Ready to Take the Next Step?

Your first home dream is closer than you think. With the right guidance, government schemes, and smart suburb selection, $35,000 can get you started.

I’ve helped hundreds of first home buyers in St George navigate this exact journey. Let me help you too.

Contact Michael Kalinovski:

Phone: 0411 81 81 71

Email: michael.kalinovski@century21.com.au

Office: Shop 1/343 Bay St, Brighton-Le-Sands NSW 2216

Website: michaelkalinovski.com

Recognised | Respected | Recommended

Helping St George families for 25+ years

About the Author

Michael Kalinovski is a St George real estate specialist with Century 21, based in Brighton-Le-Sands. With 25+ years of experience, he’s helped over 500 families buy and sell property in the St George area. Michael specializes in first home buyers, providing honest, no-pressure guidance through the buying process. He lives locally and has deep knowledge of every St George suburb.

This article was published on February 12, 2026. Property prices and government schemes are current as of this date. Always verify current schemes and eligibility with official sources.

If you found this guide helpful, please share it with friends who are saving for their first home. The more people who know about these schemes, the more first home buyers can achieve their dreams.